Maybank has taken a significant step towards boosting online banking security with the launch of Money Lock, a first-of-its-kind feature on the MAE app. This innovative tool empowers customers to take control of their finances by allowing them to “lock” specific amounts within their savings or current accounts, effectively preventing online access to those funds.

Peace of Mind with Secured Bank Balances

Money Lock addresses a growing concern for many: online scams and fraudulent activity. By adding this extra layer of protection, Maybank allows its customers to enjoy the convenience of online banking with a heightened sense of security.

The feature offers a high degree of user control. Customers can choose to lock any amount from RM10 upwards, right up to their entire account balance. This flexibility allows for tailored protection based on individual needs. Additionally, increasing locked amounts is a breeze through the MAE app, and there are no fees or restrictions on how often Money Lock can be activated.

Money Lock is the latest feature focused on creating a more secure banking environment for bankers. Malay The introduction of Money Lock in Malaysia follows the feature’s successful implementation in Singapore.

“Money Lock empowers customers with confidence,” states Syed Ahmad Taufik Albar, Group CEO of Community Financial Services at Maybank. He emphasizes that customers can conduct online transactions securely while still earning interest on their locked funds.

Unlocking Funds and Avoiding Disruptions

Unlocking requires a visit to a Maybank ATM or branch for verification, ensuring the locked funds remain secure. This step is crucial in preventing unauthorized access.

Maybank emphasizes the importance of careful financial planning before activating Money Lock. Customers should consider upcoming commitments and ensure sufficient funds are available for essential transactions to avoid disruptions.

A Multi-Layered Approach to Fraud Prevention & Security

Money Lock is one piece of a comprehensive security puzzle. Maybank highlights other measures taken to combat fraud, including replacing SMS OTP with the more secure Secure2u system, restricting online banking access to one device per customer, and implementing cooling-off periods for limit increases.

Alongside technological advancements, customer awareness remains vital in the fight against scams. Maybank encourages users to be cautious of calls and messages from unknown numbers, to only download apps from official stores, and to never share online banking credentials with anyone.

AEON Bank (M) Berhad officially launched its operations on May 26, 2024, marking a significant milestone as Malaysia’s first fully Islamic digital bank. The launch ceremony, held at AEON Hall, AEON Mall Shah Alam, was attended by prominent figures from the financial sector and government, including Yang Bahagi Datuk Johan Mahmood Merican, Secretary General of Treasury, Ministry of Finance.

From left to right: Datuk Johan Mahmood Merican, Secretary General of Treasury, Ministry of Finance; Raja Teh Maimunah, CEO of AEON Bank (M) Berhad; Daisuke Maeda, Non-Independent Executive Director of AEON Bank (M) Berhad & Chairman ofAEON Credit Service (M) Berhad; Naoya Okada, Managing Director of AEON Co (M) Berhad

AEON Bank offers a variety of Shariah-compliant digital banking solutions for personal banking customers. These currently include:

Savings Account-i: This account offers a competitive profit rate.

Savings Pots: Users can create customized savings pots to achieve specific financial goals.

Budgeting Tools: These tools help users manage their finances effectively.

Customers who activate their accounts can immediately access a virtual AEON Bank x Visa Debit Card-i. A physical debit card option is also available upon request.

AEON Bank emphasizes providing a seamless user experience. New customers signing up during the launch campaign can enjoy a 3,000 AEON Points bonus and earn triple the points on transactions using their new debit card. Additionally, existing members of the AEON Points program will have their membership automatically linked to the AEON Bank app. This integration unlocks further benefits and rewards across the extensive AEON ecosystem, encompassing AEON Malls, supermarkets, and partner merchants. Points earned can be conveniently converted to cash within the user’s AEON Bank account.

AEON Bank is committed to reaching a broad customer base. The launch campaign at AEON Mall Shah Alam featured public activations, family-oriented activities, and exclusive giveaways to engage with the community. This approach will continue with nationwide roadshows planned across eight Malaysian states from June to November 2024.

By prioritizing accessibility, AEON Bank aims to empower all Malaysians, particularly the underserved and unbanked segments, to participate in the financial system and achieve their financial goals. The launch of this Islamic digital bank is a noteworthy development in Malaysia’s evolving financial landscape.

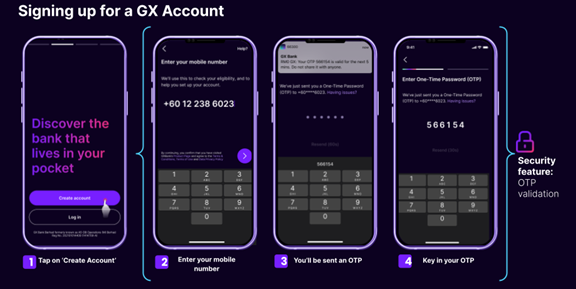

GX Bank Berhad (GX Bank) is pushing boundaries as Malaysia’s first digital bank to go to market. The digital bank received approval to operate from Bank Negara Malaysia ahead of the April 2024 deadline. The bank focuses on serving the underserved through innovative channels, including a dedicated app and 24/7 customer support.

After its initial announcement back in September, GX Bank is already rolling out its official app in beta. The beta app is set to roll out to 20,000 Malaysians on November 14, 2023, following successful internal testing. GX Bank’s app is developed to be user-centric. The app comes with a user-friendly interface prioritizing trust and security. Chief Technology Officer Fadrizul Hasani emphasizes compliance with regulatory norms, ensuring user data and funds’ safety.

During beta-testing, users can create a GX Bank Savings Account and set up to 10 “Pockets” for specific savings goals. Money placed in these pockets will earn daily interest of up to 3%. Being the first digital bank to go to market, it may be daunting to be an early adopter. That said, deposits of up to RM250,000 in GX Bank are protected by Perbadanan Insurans Deposit Malaysia (PDIM). In addition, users are able to lock their accounts in case of fraud and limit daily spending. GX Bank is also offering exciting benefits including RM20 cashback with a minimum of RM100 deposit, withdrawal fee waivers, and unlimited cashback with the upcoming debit card feature.

Simple Onboarding Process

GX Bank promises a seamless onboarding experience. With a few taps, users can download the app, complete the eKYC process, upload their MyKad, and deposit a minimum of RM10 to start saving.

To set up your account, all you need to do is:

Download the app from the Google Play Store or Apple App Store

Upload a digital copy of the national identity card (MyKad)

Complete the eKYC process as stated in the app

Add a minimum of RM10 into the savings account and set up Pockets (if you want to)

Existing Grab users can access the GX Bank app through the Grab App.

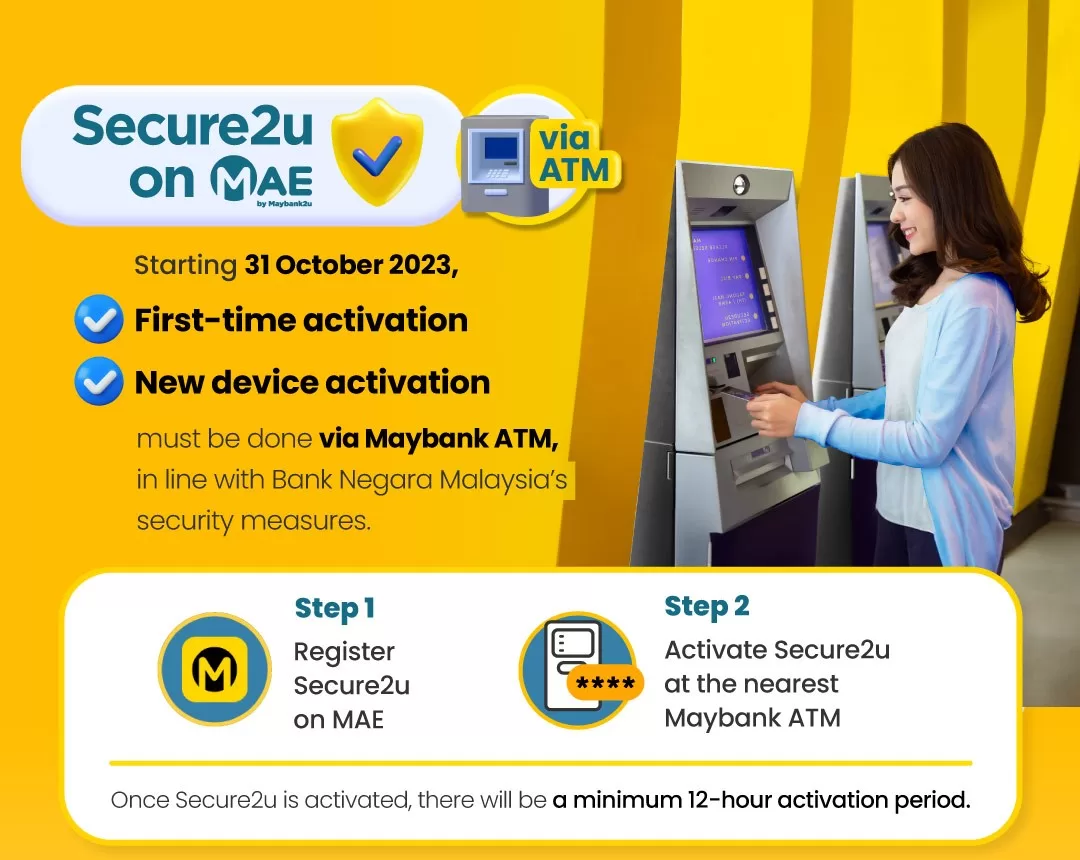

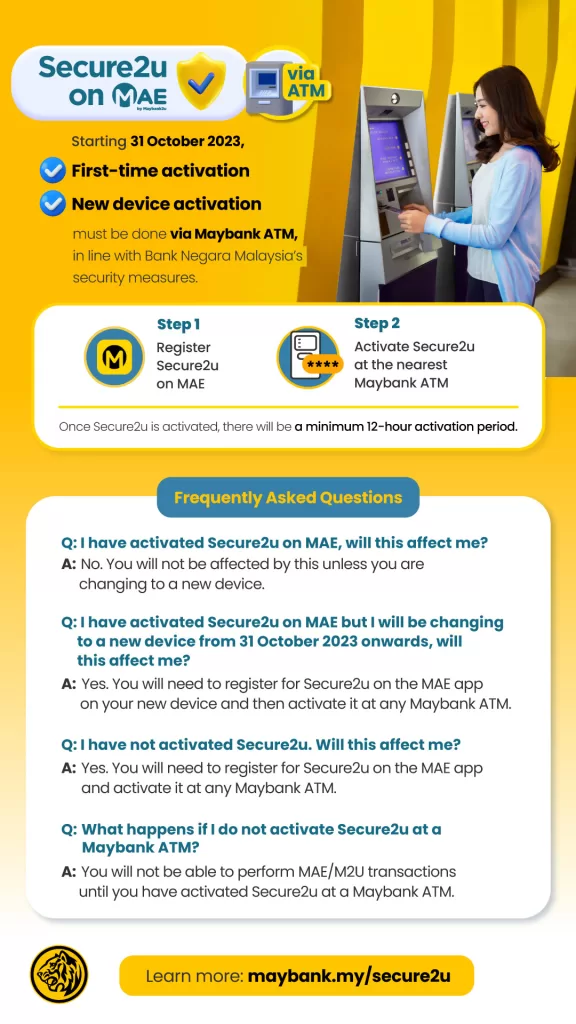

Maybank is ramping up its security measures to protect customers from unauthorized transactions and financial scams. The bank has introduced an additional verification process for its Secure2u authentication method used for online banking transactions on the MAE app and Maybank2u web.

Starting October 31, 2023, first-time Secure2u users or those accessing it from a new device can securely activate it at any Maybank ATM across Malaysia. This new measure complements the five anti-scam measures introduced by the bank in July 2023.

Dato’ John Chong, Group CEO of Community Financial Services at Maybank, explained the significance of this initiative. He stated that allowing customers to self-activate Secure2u via an ATM enables them to physically verify their identity, giving them greater control over their online banking authorization process. This not only safeguards their accounts but also their finances from potential scammers.

The activation process is simple. Customers need to follow two steps:

Register for Secure2u on the MAE app, and

Activate Secure2u using their debit, credit, or charge card PIN number at any of Maybank’s 3,000 ATMs nationwide.

Once activated via ATM, customers can begin approving transactions after a 12-hour wait period. The bank may adjust this cooling-off period based on scam trends and transaction patterns. This step ensures that customers have sole approval authority over their Secure2u registration, adding an extra layer of security.

Maybank’s extensive network of ATMs ensures easy access for customers. These ATMs operate from 6:00 AM to 12:00 AM daily and are strategically located in branches, service centres, shopping malls, petrol stations, train stations, hospitals, and more.

For a step-by-step guide on Secure2u activation and more information, visit maybank.my/secure2u.

If you checked your Touch ‘n Go eWallet app these past few days, you would have noticed a new feature, or a new icon. You might have come across ‘GO+’. I know I have, and a few of our friends have asked us what it was before today’s official launch of Touch ‘n Go’s GO+. Now that it is officially launched, we can properly explain what GO+ is.

Welcome to GO+, your gateway to small time investments and mainstream financial services. Essentially, you are investing with Principal, an asset management platform anchored by CIMB. In turn, GO+ is anchored by Principal, in alliance with CIMB, specifically their e-Cash Fund platform.

GO+ will take advantage of Principal’s asset management platform to sort of make investments to grow your financial assets via Touch ‘n Go’s eWallet platform. By putting as little as RM10 into the platform will supposedly guarantee a growth rate of 1.43% per annum. While that may not seem like much, it is more than putting your money into your bank’s savings account or current accounts.

The growth is not credited over a year long period too. You get returns on a daily basis and the returns are credited to your GO+ account every day. That also means the growth is an immediately visible one. Principal also promises no risks to the platform, so you can be rest assured that you will only be seeing growth.

What makes GO+ even better for users is that because it is integrated with Touch ‘n Go eWallet app, you can transfer the funds from GO+ into Touch ‘n Go eWallet accounts immediately at any given time, and vice versa. It does not stop there though; you can transfer credits from GO+ to any of your registered bank accounts immediately too. You can even use your GO+ account to pay for things via Touch ‘n Go eWallet app. That also means with GO+, you are more flexible than anything else you can currently find on the Malaysian market.

To get yourself on GO+ now, you can look into your Touch ‘N Go eWallet app and immediately register and upgrade your account to a GO+ account. You can start investing with GO+ with as little as RM10. For now, the service is only available to Malaysian citizens above 18 years of age. The Touch ‘n Go eWallet app is available for free from Google’s Play Store and Apple’s App Store for Android and iOS respectively

“We live in a time of great change. Thanks to technology, the rate of change around us continues to accelerate,” said Jim Whitehurst, president of IBM. Although today’s banking landscape in Asia-Pacific is proving slow to change, the springboards that could redefine banking are quickly emerging.

One such springboard is regulators issuing digital banking licenses in the region. The Hong Kong Monetary Authority, for example, gave out eight virtual banking licenses last year. Awardees include Ant SME Services (Hong Kong) Limited, Ping An OneConnect Company Limited, Tencent’s Infinium Limited, and Xiaomi’s Insight Fintech HK Limited. Depending on the country, the licenses would allow non-banking entities to conduct banking activities such as taking deposits from retail customers and giving out loans to businesses. Since such firms are not required to have physical branches, they are also called online-only, virtual, or neo-banks. Examples of virtual banks in the region that are already in operations include Tencent’s WeBank in China, and Kakao Bank in South Korea.

These new entrants, together with fintechs, have raised customers’ expectations of banking services. Recent research from independent research firm Forrester found that 77% of Asia-Pacific banking customers prefer to interact with their financial services providers on digital channels, especially in mobile-first countries such as Mainland China, India, Indonesia, and Thailand. Nearly three-quarters of them also believed that they should be able to accomplish any financial task on a mobile device.

As the incumbent banks in Asia-Pacific are finding ways to address those changes head-on, they also need to look at their IT infrastructure, which supports and enables their business models. This is because the IT infrastructure handles the most demanding compute transactions such as trading stocks, bonds, currencies, or derivatives, or allowing retail customers to make purchases using a smartphone app.

Simplifying IT to drive better business outcomes

Established banks today are running on core systems that are often inflexible, expensive to maintain, and difficult to integrate with customer channels. Moreover, while integration is necessary, it is not sufficient to be able to create the technology platform flexibility necessary to lower operating costs, adapt to changes quickly, and optimize customer engagement. To overcome these challenges, banks in Asia-Pacific are working to transform their often monolithic, rigid, legacy IT architecture to a more open architecture that provides the agility to deliver dynamic business needs. This enables them to:

Optimize operations by streamlining processes

Since a single customer record can have various finance-related transactions associated with it, banking systems based on application programming interfaces (APIs) can better service multiple activities associated with a single customer record. Banks can further improve operational efficiency by deploying an API integration tool, which connects externally facing APIs with the internal banking APIs and systems of record. It transforms and directs incoming API requests to the appropriate endpoint within the IT environment, allowing changes to the back-office without impacting customer engagement services.

Additionally, banks can leverage microservices to expose individual functions, facilitating new service implementation as well as existing service updates. A microservices-based architecture can help banks better integrate their services into their partners’ platforms to deliver more services to customers. Since microservices can be reused, they also flexibly support and maintain production services by removing single points of failure in end-to-end flows. To reap the full benefits from microservices, they should be coupled with containers, which enable the portability of decisioning systems, across hybrid cloud environments.

Consistently deliver good customer experience in a standardized way despite changes in the business

Banks were initially built based on the branch office model, and were later supported by call centers and digital channels. These changes call for the IT architecture to be enhanced so that IT can effectively support new business models. However, there might be cases where IT architects missed integrating IT enhancements or new channels with existing operations, leading to data silos.

This is where standards, which can be critical for processing within the back office, can help. They are able to provide a foundation for a uniform system blueprint that gathers more detailed and consistent customer data that can be more easily combined across different transactions and banking channels. Since banks do not have the luxury of shutting down operations to rebuild, applying consistent standards across the board helps to more easily modify processing while still running and maintaining established levels of customer support. API implementation and reuse from shared catalogs can help to enforce adherence to standards and accelerate delivery.

Support business agility through continuous delivery

As change is the only constant, banks need to be able to rapidly develop and modify servicing logic, business rules, and predictive models to adapt to changing customer demands, comply with new regulations, and respond to new competitive offerings. A modern, microservices-based architecture can help banks gain that agility by enabling them to adopt continuous integration and continuous delivery (CI/CD) so that they can build, deploy and manage apps quickly.

Open source will be key to transforming the back-office

As more banks are embarking on the modernization journey to simplify IT, they are harnessing open source solutions to support customer engagement applications and deliver delightful customer experiences. According to The 2020 State of Enterprise Open Source: A Red Hat Report, 93% of IT leaders from the financial services industry globally said enterprise open source is important to their organization, and cited IT infrastructure modernization as one of the top three use cases for the technology. Respondents cited top reasons for using enterprise open source as being able to gain access to latest innovations and achieve higher levels of security.

Thailand’s Kasikorn Bank (KBank) is one bank that has benefitted from enterprise open source. It tasked its tech arm, Kasikorn Business-Technology Group (KBTG), to update and optimize its IT infrastructure to ensure that its mobile banking app is feature-rich, user-friendly and reliable even as the user base grew. KTBG did so by deploying Red Hat’s open source solutions, including Red Hat Enterprise Linux, Red Hat JBoss Enterprise Application Platform (JBoss EAP), Red Hat AMQ, and Red Hat OpenShift Container Platform.

Coupling the tech deployment with DevOps and agile methodologies, KTBG achieved the speed and scale KBank needed such that it can now handle 5,000 transactions per second. The open, modern IT architecture also enabled KBank to easily connect with its business partners’ systems to deliver more features on its mobile banking app, and provided a responsive, reliable application environment that reduced application development time from one month to two weeks. All in all, the changes that are reshaping the financial services industry offer established banks in Asia-Pacific opportunities to adopt technology that can increase their competitiveness and agility. In response to this, banks in the region have enhanced many of their customer-facing front-end operations with digital solutions. However, the front-office experience only makes up a small part of the entire process. Most of the servicing happens on the back end, often using numerous manual touchpoints that are rarely exposed to customers. Having a digital banking platform built on enterprise open source can help banks simplify IT and break down barriers between the customer engagement and back-office teams. With a stable yet flexible platform that can scale and adapt, banks can deliver a streamlined and frictionless customer experience that meets their expectations, therefore cracking the code to becoming successful digital banks that can compete effectively with new entrants.

The way banking is being conducted around the world is changing, especially with customers who are always connected through mobile phones and with 5G not far away in many places.

Coupling that with the rising levels of wage growth entrepreneurship and government policies for financial inclusion, banking’s traditional customer journeys and distribution models won’t scale nor reach the average consumer, and will be significantly cost-prohibitive for the average bank to service. The idea that a consumer needs to visit a branch doesn’t even come into their equation.

Moreover, the consumption of banking products from FinTechs, including unsecured lending, peer-to-peer payments, merchant payments, and business credit, is on the rise. Providers like Ascend Money and Rakuten are fast, simple and digital-first. Simply put, they engender customer satisfaction.

To catch up with those competitors, many banks have embarked on digital transformation in an effort to transform their customer experiences. However, while many banks have — to some degree — a maturing “front end”, their middle and back offices are often made up of fragile and inflexible applications and data systems. Since such systems limit the bank’s ability to scale and adapt to change quickly, it prevents the front office from running efficiently, which in turn hinders banks from delivering innovative customer journeys.

Furthermore, as net interest margins will likely stay very slim, the continual pressure to make these middle and back-office systems operationally efficient is becoming a higher priority in CFO’s targets.

What are we seeing in the middle and back office in banking?

The prioritization to modernize the back-office applications, databases, and platforms in order to be agile can help re-engineer the customer journey and lower business as usual operations and change management costs. To achieve that, banks need to focus on the following areas:

IT infrastructure modernization, as most banks are still running on legacy IT systems that were deployed in silos. With business functions isolated from one another, it can be difficult for banks to deliver a seamless and consistent customer experience across various channels and services.

Digital process-driven application modernization. Many banking processes still rely heavily on manual or clunky processes to ensure compliance with policies and historic procedures. Credit adjustments, credit disputes, loan approvals, case management, fraud event management, for example, require human reviews and hand-written approval signatures. When coupled with KYC (know your customer) as a principal operating model, integrating this into manual or clunky processes is a must-have for improving customer experience.

The keys to improving operational efficiency

Taking the application and infrastructure design lessons learnt from the digital front-end services — such as being API-oriented, able to be deployed on a Linux container architecture, can scale horizontally, and have updates delivered rapidly through a microservice architecture — and applying them to the middle and back-office systems can help deliver the desired operational efficiencies.

Most banks, however, have decades of IP, rules, and processes hardcoded deep into the system, or have multiple clunky expensive business process management middleware workflow tools, each with their own proprietary extensions and interfaces. As such, modernization can be a difficult task, especially when they don’t know where to start.

Examples of success

BBVA — which operates in 30 countries with their associated regulatory jurisdictions and serves more than 72 million customers — was one bank that faced legacy issues. The bank managed to overcome these by modernizing the middle office business process and rules centric applications to be API first, easily extendable, globally reusable with consistent developer experience, scalable, container-based and open.

Capital One undertook a similar exercise with its middle office systems. Since the bank was initially using multiple case management process tools (each with their own interfaces, runtimes and toolsets), it decided to standardize and simplify its case management processes to improve its operations. By implementing an open source, API-oriented, easily scalable, and changeable case management and process management layer, Capital One managed to speed up delivery and drive down costs.

Speaking of APIs, these have typically been utilized as a software design principle for digital front ends in banking. However, having middle and back-office systems and data with an API layer across these can drive much greater operational efficiency. With customer journeys or compliance services increasingly demanding back-office systems to be integrated, what better way of connecting those systems than to leverage APIs?

The trick to doing so successfully is to design and modernize middle and back-office applications with useable and scalable APIs to integrate the digital and front office systems of engagement with.

Moreover, as these applications and databases become updated with APIs as integration points, the use of microservices can be important in improving transactional and operational efficiency. This relates to the lowering of IT infrastructure costs and driving down the cost of IT delivery year on year.

As applications are modernized with APIs and a microservice application architecture, they are often deployed on Linux containers. For the product and customer support managers in the bank looking for ways to make constant variations to their systems — either to improve the back-office process, enhance a customer experience or meet compliance — having these systems running as small componentized microservices gives their IT team the ability to roll out updates to their system without taking down the entire application. This can give the bank a higher degree of agility, while helping to save cost because it can take significantly less time and fewer people to release an update.

All in all, providing exceptional customer experiences may call for banks to transform their digital experiences beyond impressive user interfaces. APIs, microservices, and other open source solutions can help with back-end processes that are highly integrated and streamlined. With more efficient back-office operations, banks around the world will be better prepared to provide the seamless user experience that customers expect.